Copies of this publication may be obtained by calling 651-296-6753. This document can be made available in

alternative formats for people with disabilities by calling 651-296-6753 or the Minnesota State Relay Service at

711 or 1-800-627-3529 (TTY). Many House Research Department publications are also available on the

Internet at: www.house.mn/hrd/hrd.htm.

INFORMATION BRIEF

Minnesota House of Representatives

Research Department

600 State Office Building

St. Paul, MN 55155

Joel Michael, Legislative Analyst, 651-296-5057

Nina Manzi, Legislative Analyst, 651-296-5204 Updated: July 2007

Marriage Penalties and Bonuses

and the Minnesota Income Tax

The Minnesota individual income tax imposes “marriage penalties” on some

couples, while granting bonuses to other married couples. This information brief

provides background information on the treatment of marriage under the

Minnesota and federal income taxes—the history, descriptions of the provisions

that create marriage bonuses and penalties, and the possible effects of marriage

penalties and bonuses on taxpayer behavior.

Contents

Summary..........................................................................................................................................2

A Basic Introduction............................................................................................................4

The History ..........................................................................................................................6

Taxpayers Affected by Marriage Penalties and Bonuses ................................................................8

Minnesota Tax Provisions that Create Penalties and Bonuses ......................................................11

Features of Federal Law that Create Minnesota Penalties and Bonuses .......................................18

Estimates of Federal Penalty and Bonus Amounts........................................................................20

Behavioral Effects of Penalties and Bonuses.................................................................................22

Appendix A: An Outline of the History of the Treatment of Marriage

Under the Federal Income Tax ..........................................................................................24

Appendix B: Treatment of Marriage Under Other States’ Income Taxes.....................................27

House Research Department Updated: July 2007

Marriage Penalties and Bonuses and the Minnesota Income Tax Page 2

Summary

Introduction. Marriage penalties and bonuses are common under the federal and Minnesota

income taxes. A marriage penalty occurs when a married couple pays higher tax than they

would if each spouse could file as a single and pay tax on his or her own income. A bonus

occurs when they pay lower tax as a married couple than they would if they filed as singles.

Penalties and bonuses result from (1) the requirement that married couples pay tax on their joint

income, (2) the progressive rate schedule, and (3) dollar limits on deductions and credits. (See

pages 4 to 5.)

It is not possible to design an individual tax that:

• is progressive (i.e., the proportion of income paid in tax increases as income rises);

• is marriage neutral (tax does not change when two individuals marry); and

• taxes married couples with the same incomes equally.

Thus, the legislature must make tradeoffs among these three goals in structuring the income tax.

(See page 5.)

History. Both the Minnesota and federal income taxes began as taxes that applied separately to

each spouse’s income and deductions. As a result, they were marriage neutral. The Minnesota

tax followed this pattern from 1933 through 1984. From 1985 through 1998, the Minnesota tax

followed an approach that taxed married couples with the same incomes equally, but the tax was

not marriage neutral. It provided bonuses to some couples and imposed penalties on others. In

1999 Minnesota implemented a marriage credit to offset the portion of the penalty in the state’s

rate and bracket structure resulting from the distribution of earned income among spouses.

The federal tax presently taxes married couples with the same incomes equally, but the tax is not

marriage neutral. For more than 20 years (1948 to 1969), the federal tax followed a pattern of

equal taxation of married couples in which nearly all married couples received bonuses. The

Minnesota tax never used this regime. Beginning in 2001, federal legislation has reduced

penalties (and provided bonuses) by increasing the married joint standard deduction relative to

the single deduction and by setting the income bracket for married joint filers for the lowest tax

rate at twice the level for single filers. (See pages 6 to 8.)

Taxpayers affected by marriage penalties and bonuses. Although particular circumstances

may lead to different results, some general rules about how couples are affected by penalties and

bonuses include the following (see pages 8 to 11):

• One-earner couples generally receive bonuses

• Couples pay penalties if each spouse earns about half of the family’s income

• Low-income couples with children are more likely to pay large penalties

• Middle and higher income couples where each spouse earns income are likely to pay

penalties

House Research Department Updated: July 2007

Marriage Penalties and Bonuses and the Minnesota Income Tax Page 3

Minnesota tax provisions that create penalties. Nine Minnesota income tax provisions can

result in marriage penalties or bonuses (depending upon the circumstances of the couple):

• Elderly exclusion

• Education deduction

• Charitable contribution deduction for nonitemizers

• Tax rate and bracket structure

• Dependent care credit

• Education credit

• Long-term care credit

• Working family credit

• Alternative minimum tax (AMT) exemption amount

• AMT exemption phaseout

The largest per-couple penalties (in dollar amounts) result from the working family and

education credits. These penalties can exceed $2,000 per couple. The individuals affected by

these credits are lower income taxpayers. The AMT provisions also impose large penalties. It is

not clear how many taxpayers are actually affected by these large penalties. The largest

(theoretical) bonuses result from the working family credit. (See pages 11 to 18.)

Federal law provisions that create Minnesota penalties and bonuses. A large number of

features of the federal income tax create penalties and bonuses that carry over to Minnesota law.

These result because Minnesota uses federal taxable income as the starting point for its tax base.

These federal penalties generally result from dollar limits on deductions or other tax features

used to calculate federal taxable income. (See pages 18 to 19.)

Estimates of federal penalty and bonus amounts. A Congressional Budget Office study and a

study by Treasury Department economists have estimated the amount of federal marriage

penalties and bonuses. These two studies reach slightly different results, but find that about half

of married couples receive bonuses while half pay penalties. The dollar amounts of penalties and

bonuses are about equal. At this point, data is not available to prepare similar estimates for the

Minnesota tax. It seems safe to conclude that Minnesota penalties and bonuses would follow the

federal pattern, but would be significantly smaller, both in absolute terms and relative to the

amount of Minnesota tax. (See pages 20 to 22.)

Behavioral effects of penalties and bonuses. Studies by economists suggest that marriage

penalties and bonuses may affect taxpayer behavior. Penalties are most likely to reduce the

amount of work by secondary-earning spouses. Studies have reached conflicting results on

whether they affect the decision to marry or divorce. At a minimum, penalties appear to cause

some couples to delay getting married. (See pages 22 to 23.)

House Research Department Updated: July 2007

Marriage Penalties and Bonuses and the Minnesota Income Tax Page 4

A Basic Introduction

The federal and Minnesota income taxes impose marriage penalties on some married couples,

while granting bonuses to other married couples. Marriage penalties and bonuses result from the

following features of the income tax:

• Joint filing by married couples

• Progressive tax rates

• Dollar limits on deductions and credits

Both the federal and Minnesota income taxes produce marriage penalties and bonuses

because couples generally pay tax under a progressive rate structure on their joint incomes.

As has been widely recognized, when two individuals marry, their combined income tax

frequently changes. It may increase, resulting in a marriage “penalty,” or it may drop, yielding a

marriage “bonus.” Penalties and bonuses occur both under the federal and Minnesota income

taxes. They result because both taxes effectively require the spouses to combine their incomes in

calculating tax.

1

Joint filing and reporting of income interact with other features of the tax,

particularly the progressive tax rate schedule and the dollar limits on deductions and credits, to

produce marriage penalties or bonuses. The examples in the boxes on this page and the next

illustrate how the Minnesota tax can result in marriage penalties for some couples and bonuses

for others.

Example of a Marriage Penalty

H and W each earn $35,000 and claim the standard deduction. If they can file as singles, each will have

Minnesota tax liability of $1,488 or a combined tax of $2,977 for tax year 2007. If H and W marry and

file a joint return, their combined tax increases to $3,172, resulting in a marriage penalty of $195.

The marriage penalty occurs because the married joint tax brackets are not twice the width of the single

brackets. For a single filer, the first $20,310 of income is taxed at 5.35 percent, and income from

$20,311 to $69,990 at 7.05 percent. Thus as single filers, H and W would have $42,620 of their income

taxed at the 5.35 percent rate (i.e., twice the bracket for single filers) and the rest of their income taxed

at 7.05 percent. As a married joint filer, the first $31,150 is taxed at 5.35 percent and additional income

at 7.05 percent. As a result, H and W will have $11,470 more ($42,620 - $31,150 = $11,470) of their

income taxed at 7.05 percent, rather than 5.35 percent. This accounts for the $195 marriage penalty.

As described in the text, the marriage credit addresses this marriage penalty.

2

1

A married couple may file separate federal returns with each spouse separately reporting his and her income

and deductions. However, doing so nearly always results in a higher total tax liability. Minnesota law requires

taxpayers to file using the same filing status that they do for federal purposes. Minn. Stat. § 289A.08, subd. 6.

2

Before tax year 2003 and in tax year 2005, H and W would have faced an additional marriage penalty under

the Minnesota income tax as a result of the standard deduction for married joint filers being smaller than that

allowed for single filers. As a result, marriage resulted in a combined reduction in the standard deduction compared

with filing singly.

The federal Economic Growth and Tax Relief Reconciliation Act (EGTRRA) of 2001 put the

marriage penalty in the standard deduction on a schedule to gradually phase out by tax year 2009. The federal Jobs

Growth Tax Relief Reconciliation Act (JGTRRA) of 2003 temporarily accelerated the married joint standard

deduction to equal twice the single deduction for tax years 2003 and 2004 only. Minnesota conformed to the

EGTRRA 2001 and JGTRRA 2003 changes. The federal Working Families Tax Relief Act of 2004 (WFTRA)

further accelerated the schedule so that the married joint standard deduction would equal twice the single deduction

House Research Department Updated: July 2007

Marriage Penalties and Bonuses and the Minnesota Income Tax Page 5

Example of a Marriage Bonus

W earns $70,000 and claims the standard deduction. H has no income and no tax. W’s tax as a single

filer would be $3,956. Marriage to H will reduce the tax to $3,172, a marriage bonus of $784. Three

factors account for the bonus:

The standard deduction for married joint filers is $10,700, while the deduction for a single

filer is $5,350; as a single filer, W could claim only $5,350. Since H had no income, he

received no tax benefit from the standard deduction. As a result, marriage reduced W’s

taxable income by $5,350 ($10,700 - $5,350 = $5,350). Since this income would have

been taxed at 7.05 percent, it accounts for $377 of the bonus.

An additional personal exemption of $3,400 is available. H had no income and derived no

benefit from the exemption; marriage allows H’s personal exemption to reduce W’s taxable

income. Since this income would have been taxed at 7.05 percent, the personal exemption

accounts for $240 of the bonus.

More income is taxed at the 5.35 percent rate. As a single filer, W’s first $21,310 of

income is taxed at 5.35 percent. Marriage increases this to $31,150. As a result, W will

have $9,840 more of her income ($31,150 - $21,310 = $9,840) taxed at 5.35 percent, rather

than 7.05 percent. This accounts for $167 of the bonus.

It is impossible to design a tax that (1) is marriage neutral, (2) is progressive, and (3) taxes

married couples with equal incomes equally. It is useful to consider marriage penalties and

bonuses in terms of the goals of an income tax system. Many, if not most, observers would

agree that in the context of marriage, the tax should satisfy three goals:

• Progressivity. Under a progressive tax, tax increases as a percentage of income as

income increases. Progressivity can be achieved through a graduated rate structure, by

providing a fixed per person or family deduction or exemption, or other features.

• Marriage neutrality. Marriage should not increase or decrease the amount of tax two

individuals pay. The tax should be marriage neutral.

• Equal taxation of married couples. Under this principle, married couples with equal

ability to pay should pay the same tax. This principle probably has the least widespread

acceptance of the three principles. It assumes that a married couple is the appropriate

taxpaying unit for measuring ability to pay.

The three principles cannot all be simultaneously satisfied; they conflict. For example, a tax

system can be marriage neutral and progressive, or married couples can be taxed equally and the

tax can be progressive. But it is impossible to satisfy fully all three principles.

3

As a result,

for tax years 2005 through 2010. Minnesota did not conform to WFTRA until tax year 2006, so that Minnesota’s

income tax included a marriage penalty resulting from the standard deduction in tax years before 2003 and in tax

year 2005.

3

This inconsistency can be demonstrated algebraically. See, e.g., Joint Committee on Taxation, The Income

Tax Treatment of Married Couples and Single Persons, 96

th

Cong., 2d Sess., 1980, Committee Print 26, 1, or

Congressional Budget Office (CBO), For Better or Worse: Marriage and the Federal Income Tax, June 1997, 3-4.

House Research Department Updated: July 2007

Marriage Penalties and Bonuses and the Minnesota Income Tax Page 6

Historical Highlights of the Federal Income Tax

Treatment of Marriage

1913-1948: Single filing; marriage neutrality. The

federal tax began by favoring marriage neutrality. The tax

applied to individuals, not married couples. Spouses were

taxed separately on their earnings and the income from

their property. Marriage was largely irrelevant.

1948-1969: Equal taxation of couples with marriage

bonuses. Court cases in the 1930s and 1940s held that

married couples in community property states (mainly

states that derived their property laws from the Spanish

civil law tradition) could split their incomes. This reduced

the tax of most couples, since more income was taxed in

lower brackets. In 1948, Congress permitted all married

couples to file joint returns with income splitting, i.e., the

married joint brackets were twice the width of the single

brackets. As a result, most couples received bonuses.

1969-present: Mixed system of marriage penalties and

bonuses. Many single taxpayers perceived joint filing and

income splitting as a “singles penalty.” Marriage bonuses

meant that marriage usually reduced tax, sometimes

substantially. Congress responded in 1969 by expanding

the width of the brackets for single filers. This created a

system in which some couples paid marriage penalties,

while others received bonuses. The exact result depended

upon the split in income between the two spouses. This

system in various forms has persisted to the present.

policymakers must compromise or trade-off these goals or principles against one another in

designing the tax system. Over the history of the state and federal income taxes various trade-

offs have been made.

The History

Both the federal and Minnesota taxes have varied historically in how married couples are

taxed.

Congress and the Minnesota Legislature have made various compromises to resolve these

competing goals. The trade-offs have been made largely between the goals of marriage

neutrality and equal taxation of married couples. Highlights of the history of the federal income

tax’s treatment of marriage are listed in the box and more details are provided in Appendix A.

The Minnesota income tax has had two different regimes in its taxation of married couples.

These have more or less followed the pattern of the federal changes (see box), but the timing has

not followed the federal pattern.

4

• 1933 to 1984: Marriage

neutrality. As with the federal

income tax, the Minnesota tax

began as a tax on individuals.

Each spouse reported earnings

and income from property and

paid tax on this income under

one rate schedule. Marriage did

not affect the amount of taxes

owed. In 1971, the legislature

allowed married couples to file

combined returns. This allowed

spouses to file one return and to

apportion deductions and income

from jointly held assets between

them. Authority to allocate

property income and deductions

would generally reduce their tax,

since income could be allocated

to the spouse with the lower

income and deductions to the

spouse with the higher income.

As a result, more income would

be taxed at lower rates. The

ability to apportion income and

4

The Minnesota tax never allowed full income splitting, which was the federal regime from 1948 through

1969.

House Research Department Updated: July 2007

Marriage Penalties and Bonuses and the Minnesota Income Tax Page 7

deductions provided some married couples with small marriage bonuses.

• 1985 to 1998: Equal taxation of married couples with penalties and bonuses. The

system of individual filing continued until 1985. As part of a major individual income

tax reduction and restructuring, Minnesota adopted the then federal model of joint filing

with brackets that were less than twice the width of the brackets for single filers. (The

ratios of the state tax bracket widths more or less paralleled that used in the federal

income tax.) These changes were adopted to respond to two policy concerns. First,

individual filing considerably complicated filing and tax compliance for married couples.

As compared with federal law, income had to be disaggregated and assigned to each

spouse and deductions needed to be divided. Second, one-earner couples in Minnesota

paid considerably higher tax burdens than similar couples in many other states. The

taxation of these couples was regularly pointed out in legislative debates as one of the

major problems with the Minnesota income tax.

Adoption of the joint filing system resulted in married couples paying penalties or

receiving bonuses under the Minnesota tax. Two years later in 1987, the Minnesota tax

was again restructured in response to the federal Tax Reform Act of 1986. Tax reform

reduced the number of tax brackets to three from 15 and flattened the rate structure. The

net result was to reduce the amount of marriage penalties and bonuses.

• 1999 to present: Equal taxation of married couples, with penalties and bonuses;

marriage credit provided to offset penalties resulting from distribution of earned

income between spouses. The credit is based on the earned income of the lesser-earning

spouse, and the taxable income of the couple. The credit as enacted in 1999 defined

“earned income” as wages and self-employment income; this definition was expanded to

include taxable pension and Social Security income, which are reported separately to

each spouse and generally reflect an individual’s earning history. A credit formula in

statute calculates the amount of penalty resulting from lesser-earning spouse’s earned

income, and a table in the income tax instructions allows taxpayers to easily look up their

credit.

The credit was developed during the 1999 legislative session. Initial legislation proposed

increasing the brackets for married joint filers to be twice the width of the brackets for

single filers. While increasing the married joint brackets would have eliminated penalties

for the 350,000 Minnesota couples who faced them, it also would have increased

marriage bonuses for other filers. In conjunction with rate reductions proposed in 1999,

setting the married joint brackets at twice the width of the single brackets would have

cost an estimated $106 million in tax year 1999. Over half this cost—$58 million—

would have gone to provide bonuses, with the remaining $48 million removing penalties.

Budget constraints led lawmakers to seek a less costly way to address the issue, and the

discussion focused on a credit that would remove the penalties without increasing

bonuses. The marriage penalty credit that developed consisted of a table that provided a

credit roughly equal to the penalty faced by couples at different income levels. The credit

offsets penalties under the rate and bracket system, but does not provide bonuses. The

House Research Department Updated: July 2007

Marriage Penalties and Bonuses and the Minnesota Income Tax Page 8

estimated cost for the credit was $48 million in tax year 1999, $58 million less than the

estimate for doubling the brackets.

There is no consensus among tax experts or policymakers on the most equitable way to

treat marriage or families under a progressive income tax.

Tax experts do not agree on the appropriate way to tax married couples under a progressive

income tax. One leading commentator has characterized some of these issues of family taxation

as “insoluble dilemmas.”

5

This lack of consensus on a “right” solution suggests why over time

the federal and state taxes have gone through such significant changes in the way they tax

married couples.

6

Furthermore, standard equity principles—horizontal and vertical equity

7

—

provide little or no guidance as to what the appropriate taxpaying unit should be to measure

“ability to pay,” whether each individual is taxed on his or her income, the married couple on

their joint income, or some other arrangement.

Taxpayers Affected by Marriage Penalties and Bonuses

Three factors—(1) how income is divided between the two spouses, (2) the level of income,

and (3) the presence of children—largely determine whether the couple will pay a marriage

penalty, receive a bonus, or be unaffected.

A variety of factors affect whether a couple pays a marriage penalty or receives a marriage

bonus. As will be seen in the next section, marriage penalties and bonuses result from a complex

series of factors. However, it is still possible to posit some simple rules of thumb about which

types of married couples receive bonuses or pay penalties.

Three factors appear to be the most important:

• The division of income between the spouses. In general, a couple is more likely to pay

a penalty if the couple’s unearned income is more equally split between the two spouses.

By contrast, a one-earner couple is more likely to receive a bonus.

8

These effects result

from the rate and bracket structure. Most one-earner couples will benefit from the wider

rate brackets; more of their income will be taxed at the lower rates (either 5.35 percent or

5

B. Bittker, “Federal Income Taxation and the Family,” Stanford Law Review 27, no. 6 (1975): 1389, 1419.

6

Taxes in foreign counties also vary, reflecting the lack of consensus. The most common pattern, however, is

taxation of individuals, rather than married couples or families. See CBO, For Better or Worse, 59-60, for a

description and table classifying the income taxes in developed nations. Only eight countries use joint income or

family income, while 19 counties use individual taxation.

7

The two standard principles are horizontal equity and vertical equity. Horizontal equity is the principle that

people in equal situations should be taxed equally. Vertical equity focuses on the taxation of people with different

incomes.

8

One-earner couples refer to the “traditional” couple in which one spouse works outside of the home and earns

nearly all of the income and other stays home, typically caring for children. It should be viewed more broadly to

include couples where most income, including unearned or property income, is concentrated in one spouse.

House Research Department Updated: July 2007

Marriage Penalties and Bonuses and the Minnesota Income Tax Page 9

7.05 percent).

9

The couples with more equal income splits will have more income taxed

at higher rates, because the bracket widths for married joint filers are not twice that for

single filers. To the extent the income is included in the state’s definition of “earned

income” penalties at the state level will be offset by the marriage penalty credit.

• The couple’s overall income level. The total income level of the couple is important to

marriage penalties and bonuses. Lower income couples are more likely to be subject to

penalties (or receive bonuses) from various credits that are available to lower income

families—the working family credit, the dependent care credit, and the K-12 education

credit. By contrast, high-income couples are more likely to be subject to penalties or

receive bonuses under the rate and bracket structure.

• Whether the couple has dependent children. The presence of children is important,

since it affects eligibility for various credits that may result in marriage penalties and

bonuses, the higher working family credit for filers with children, the dependent care

credit, and the education credit.

Using these factors, it is possible to establish some general rules of thumb. These are gross

generalizations but can be useful in judging which groups of taxpayers are most affected by the

current regime of taxing married couples and single individuals. There will be a fair number of

couples in the categories who are exceptions to these generalizations because of special

circumstances. These rules of thumb are summarized in the matrix and in the bulleted

paragraphs following the matrix.

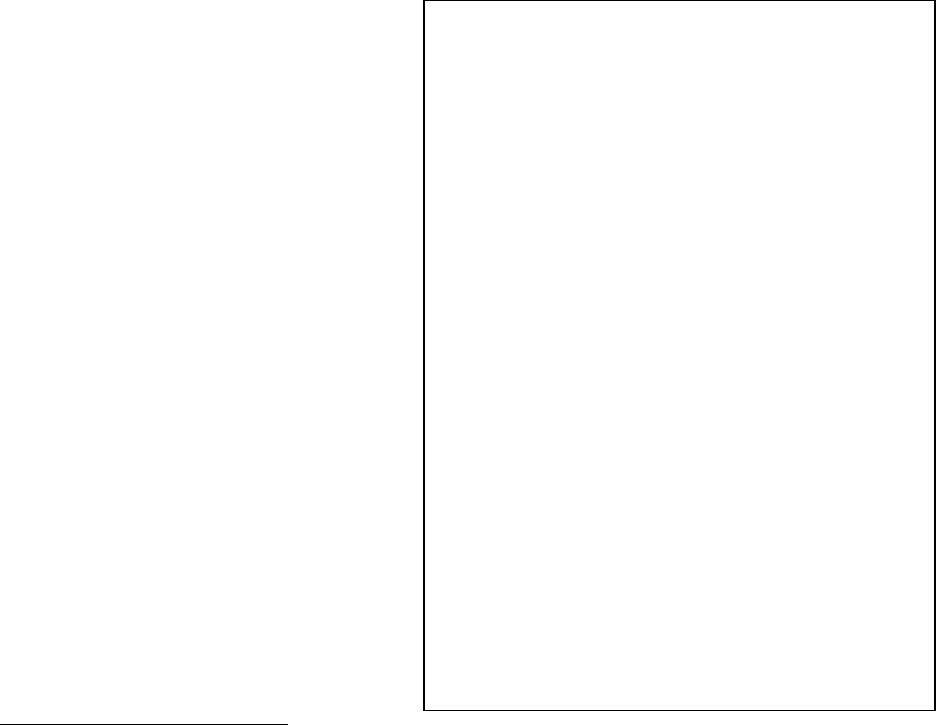

General Rules on Probability of Marriage Penalties and Bonuses

Married couple by

income and income split

No Dependents Dependents

Low-income

One-earner Bonus Bonus

Split-income Small penalty Large penalty

Middle-income

One-earner Bonus Bonus

Split income Small penalty Small penalty

High-income

One-earner Bonus Bonus

Split-income Penalty Penalty

• One-earner couples are likely to receive bonuses at all income levels, whether or not

they have children. Dependent children will generally increase the probability that

bonuses are received. Marriage may enable these individuals to qualify for the working

9

One-earner couples also benefit from personal examples for the spouse with no income. If they do not

itemize deductions, they benefit from the higher standard deduction amount for married joint filers. Both of these

features are provisions that carry over from federal law.

House Research Department Updated: July 2007

Marriage Penalties and Bonuses and the Minnesota Income Tax Page 10

family credit, a higher standard deduction, additional personal exemptions, and taxing of

more income at the 5.35 percent rate. These generalizations also tend to be true for

couples where one spouse has most of the income (e.g., 75 percent or more).

• Lower income couples with relatively equal income splits and dependent children

are subject to the largest marriage penalties, both in dollar terms and as

percentages of their incomes. These couples can suffer very large penalties because

combining the two spouse’s incomes can result in loss of various low-income credits—

the dependent care credit, working family credit, and education credit. Marriage also

reduces the standard deduction and decreases the amount of income that is taxed in the

5.35 percent bracket. This is especially so, since many of these taxpayers would qualify

to file as heads of household. Head of household filers receive larger standard deductions

and have wider tax brackets than single filers. The marriage penalty credit calculation is

based on the difference between the single brackets and the married joint brackets; the

credit will reduce but not eliminate penalties that result when a head of household filer

marries a single filer. The marriage penalty credit does not address the loss of low-

income credits.

• Lower income couples with no children and relatively equal income splits generally

will have small penalties at the federal level, or be unaffected at the state level due to

the marriage penalty credit. Couples with more equal income splits (say 50-50 or 60-

40) will typically have small marriage penalties because their standard deduction is

reduced and, in some cases, more income will be taxed at 7.05 percent, rather than 5.35

percent. Couples with slightly larger income splits (more than 60-40 and less than 75-25)

will have smaller penalties or may be unaffected. These penalties, although small in

dollar amounts, may be larger in percentage terms than the penalties higher income

couples experience.

• Middle-income couples with relatively equal income splits generally will be subject

to small marriage penalties. These couples with total incomes under $100,000

generally have some additional income taxed at higher rates because of the relative

widths of the married and single tax brackets. To the extent these couples’ income

consists mostly of earnings, the penalties at the state level will be offset by the marriage

penalty credit. Most of these couples itemize and, thus, are unaffected by the difference

in the standard deduction amounts for married, single, and head of household. Since

many couples fall into this category, a large number of small penalties add up to a large

amount of revenue.

• Higher income couples tend to be subject to small marriage penalties. These couples

will have more income taxed at higher rates because of the relative widths of the married

and single tax brackets. This is so, almost without regard to the split in income, unless

the second spouse’s income is very small. The penalties are small, especially compared

to the couples’ income. In addition, these couples may be subject to marriage penalties

that carry over from the federal income tax, such as the phase-out of itemized deductions

and personal exemptions.

House Research Department Updated: July 2007

Marriage Penalties and Bonuses and the Minnesota Income Tax Page 11

•

Couples with income splits who are subject to the alternative minimum tax (AMT)

will almost always pay marriage penalties. This is so because of the difference in the

married and single exemption amounts and because one spouse’s income may subject the

other to the AMT. These penalties are much larger than those under the regular rate and

bracket structure, and are not offset by the state’s marriage penalty credit.

10

Minnesota Tax Provisions that Create Penalties and Bonuses

Nine features of the Minnesota individual income tax create marriage penalties or bonuses.

This section of the information brief discusses provisions of the Minnesota income tax that may

cause individuals who marry to pay a higher Minnesota income tax. The next section discusses

marriage penalties or bonuses under the Minnesota tax that derive from the use of federal taxable

income (FTI) or federal adjusted gross income (AGI) to computing Minnesota tax. The

provisions included in this section are specific to the Minnesota tax structure and are not carried

over from federal law.

11

The section also calculates the theoretically maximum marriage penalty

and bonus for each of the provisions.

12

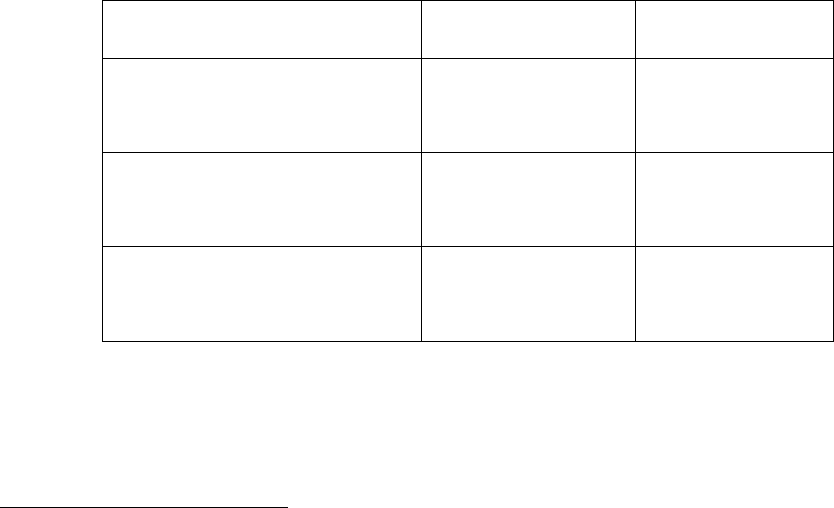

The following table lists the provisions and maximums.

The provisions are listed in the order in which they occur in computation of the income tax—i.e.,

deduction from federal tax income first, application of the rates, and finally tax credits.

10

The AMT tends to apply to taxpayers with large amounts of preference items (e.g., home mortgage interest,

property taxes, accelerated depreciation, and so forth.)

11

The provisions carried over from federal law can cause substantial marriage penalties and bonuses.

However, they can only be changed by decoupling from federal law or by otherwise adopting provisions that further

complicate calculation of, compliance with, and administration on the Minnesota tax. These issues are discussed in

the next section.

12

The amounts are theoretical maximums, since it is not clear if any couple has the specific circumstances

necessary to realize the maximum penalty or bonus. In some instances, fairly unusual or atypical circumstances may

be required to reach the maximum penalty or bonus. Nevertheless, the maximums may be useful to point out the

outer limits or parameters for the penalties and bonuses of each provision.

House Research Department Updated: July 2007

Marriage Penalties and Bonuses and the Minnesota Income Tax Page 12

Provisions of the Minnesota Income Tax

Creating Marriage Penalties and Bonuses, Tax Year 2007

Provision Maximum Penalty Maximum Bonus

Calculation of taxable income

Elderly exclusion $445 $437

Education deduction per dependent K-6 None 128

Education deduction per dependent 7-12 None 196

Charitable contribution deduction for nonitemizers None 20

Tax Rates

Couples with no dependents 325 597

Couples with dependents 692 230

Tax credits

Dependent care credit 1,440 None

Education credit 1,000 times

number of

children

None

Long-term care credit None 100

Working family credit 3,302 1,651

Alternative minimum tax exemption 1,997 995

Alternative minimum tax exemption phaseout 1,200 600

Elderly Exclusion

The elderly exclusion allows a deduction to individuals who are 65 years of age or older or who

are permanently disabled. The amount of the deduction equals a flat amount that varies by filing

status and whether one or both spouses are 65 or older or disabled. The amounts are listed

below.

13

Filing Status Exclusion Amount

Married joint $12,000

Married separate 6,000

Single 9,600

The exclusion is reduced by two additional amounts: (1) the amount of Social Security and

railroad retirement benefits that are exempt from taxation and (2) one-half of the amount of

adjusted gross income (AGI) over thresholds that vary by filing status. The thresholds are listed

below.

13

For disabled individuals, who are under age 65, the exclusion may not exceed the amount of disability

income.

House Research Department Updated: July 2007

Marriage Penalties and Bonuses and the Minnesota Income Tax Page 13

Filing Status AGI Threshold

Married joint both spouses over

65 or disabled

$18,000

Married separate 9,000

Single or married and only one

spouse over 65 or disabled

14,500

The elderly exclusion can create marriage penalties in three different ways.

• The initial exclusion amount for married joint filers is not twice the exclusion amount for

single filers. The exclusion for single filers is $9,600, while for married joint filers it is

$12,000 (compared with $19,200 for two single filers). As a result, marriage by two

qualified individuals will reduce the initial exclusion amount.

• The subtraction of nontaxable Social Security benefits (or other retirement or disability

benefits) may result in marriage reducing the available exclusion. One spouse may

receive no Social Security benefits, while the other spouse may receive Social Security

benefits that reduce or eliminate the total elderly exclusion available to the couple (as

compared with that available to them if they were able to file as singles).

14

• The AGI thresholds for married joint filers are not twice the thresholds for single filers.

As a result, marriage can increase the subtraction for income over the threshold, as well

as reducing the initial subtraction amount.

The elderly exclusion can also produce marriage bonuses. These occur when marriage enables

the couple to qualify for or receive a larger elderly exclusion. This will happen most commonly

when an individual with positive taxable income who is under age 65 marries someone with little

or no income who is over age 65. This occurs because the initial exclusion amount for married

joint taxpayers is the same ($12,000), regardless of whether one or both spouses are 65 or older.

The maximum marriage penalty as a result of the elderly exclusion equals $445.

15

The maximum

marriage bonus as a result of the elderly exclusion is $437.

16

14

Marriage can result in complete loss of the elderly exclusion as a result of the Social Security offset.

Assume C (age 65) has $14,500 of income from taxable sources and no Social Security benefits. She pays no state

income tax, since the elderly exclusion fully offsets any income remaining after the personal exemption and standard

deduction are taken. Assume she married B (also age 65) who has $12,000 in nontaxable Social Security benefits.

The marriage makes the elderly exclusion unavailable, since nontaxable Social Security benefits exceed the initial

exclusion amount ($12,000). However, the Social Security program will provide C an offsetting bonus in the form

of spousal Social Security benefits equal to one-half of B’s benefits.

15

This represents full loss of a maximum exclusion amount of $8,317 for taxable year 2006. Although the law

permits an initial subtraction amount of $9,600, it is impossible for a single elderly individual to claim this amount.

The AGI offset begins to reduce the $9,600 amount before taxable income (taking into account the personal

exemption, standard deduction, and additional standard deduction for the elderly) can reach $9,600.

16

For example, assume C, an individual who is under 65, has $25,667 of AGI. C marries B who is 65 and has

no income. The net result is (aside from the marriage bonus resulting from the rate brackets) that the couple

qualifies for a $8,167 elderly exclusion. This is a maximum exclusion and yields a tax benefit of $437 for tax year

House Research Department Updated: July 2007

Marriage Penalties and Bonuses and the Minnesota Income Tax Page 14

Education Deduction

The law allows taxpayers to deduct amounts spent for qualifying dependent education expenses.

The law specifies maximum dollar amounts per dependent of $1,625 for kindergarten through

sixth grade, and $2,500 for seventh through 12th grade. Because there is no overall limit per

filer or family, the education deduction cannot result in a marriage penalty. However, it may

create a marriage bonus. This could occur because the value of the dependent education

deduction depends upon having positive taxable income and the marginal tax bracket. Marriage

may result in the deduction exempting income from taxation or in reducing the tax rate that

applies.

17

The maximum marriage bonus is $128 per dependent in grades kindergarten through six and

$196 per dependent in grades seven through 12. The law does not limit the number of

dependents for whom expenses may be deducted.

Tax Rate and Bracket Structure

The width of the rate brackets for married joint filers is not twice the width of brackets for single

filers.

18

Thus, two single individuals who marry may have more income taxed at the 7.05 percent

and 7.85 percent rates, resulting in a marriage penalty. If the income of the lesser-earning spouse

comes entirely from earnings, this penalty will be offset by the marriage penalty credit, but the

credit will not reduce penalties that result if the lesser-income spouse has primarily unearned

income (dividends, capital gains, interest). Conversely, if one of the individuals has most or all

of the combined income, marrying may result in more income being taxed in the lower 5.35

percent or 7.85 percent rate brackets. In this case, the rate and bracket structure provides a

marriage bonus.

The maximum amount of the potential penalty equals $325 for tax year 2007. This computation

assumes that both spouses filed as singles, and that the income of the lesser-income spouse is

entirely unearned. If one of the spouses could file as a head of household, and the lesser-income

spouse had only unearned income, the penalty would increase to $692.

19

The maximum amount

2007. At higher levels of AGI, the exclusion is reduced, while at lower levels of AGI the amount of the exclusion

exceeds taxable income, yielding no additional tax benefit. This assumes the couple claims the standard deduction.

The result would be different, if they had itemized deductions.

17

This can be illustrated with an example. C has a dependent in high school and $2,500 of expenses qualifying

for the dependent education deduction. C’s taxable income puts him in the 5.35 percent bracket. The value of the

dependent education deduction to C as an unmarried taxpayer is $134 (2,500 x 5.35% = 134). He marries B whose

income is high enough to put her in the 7.85 percent bracket. C and B’s joint income is sufficient to put them in

7.85 percent tax bracket. The dependent education deduction is now worth $196 (2,500 x 7.85% = 196). They

receive a marriage bonus of $62 as a result of the increased tax value of the dependent education deduction.

18

In addition, if one or more of the spouses would have qualified for head of household tax status, the potential

penalty could be larger. Head of household is the status typically used by single parents. Given this scenario, a

penalty occurs because the rate brackets for married joint filers are not twice the width of those for head of

household filers.

19

The penalty amount would increase further if one assumes that both spouses could file as head of

households. However, in order to do so, they would be required to maintain separate households. See Treas. Reg. §

1.2-2(d) (single individual must pay one-half of the cost of maintaining household to qualify to file as a head of

House Research Department Updated: July 2007

Marriage Penalties and Bonuses and the Minnesota Income Tax Page 15

of the potential bonus equals $597 for tax year 2007. If the spouse with income could file as a

head of household, the maximum bonus drops to $230.

Dependent Care Credit

The income tax allows a refundable tax credit for child care expenses incurred to enable the

taxpayer to work. The amount of the credit is based on the federal dependent care credit. The

maximum credit is $720 for one dependent and $1,440 for two or more dependents. This

maximum credit is reduced or phased out by $18 for each $350 ($36 for two or more

dependents) of household income over $21,880 (for tax year 2007).

The Minnesota dependent care credit can result in marriage penalties. Marriage (and joint filing)

may increase the amount of household income subject to the phaseout, reducing the credit

amount.

20

Because the credit is refundable, it generally will not result in a marriage bonus.

(Nonrefundable credits can provide marriage bonuses, because one spouse may not have

sufficient tax liability to take full advantage of the credit. Marriage, thus, can increase the total

amount of credit allowed to the couple. Refundable credits do not confer these bonuses, by

contrast.)

The maximum marriage penalty under the dependent care credit is $1,440, the full amount of the

credit.

21

Education Credit

The Minnesota income tax allows parents to claim a credit for qualifying education expenses of

$1,000 per child in grades K-12, with no limit on the number of children for whom the credit

may be claimed.

22

The credit phases out when income exceeds $33,500, at the rate of $1 for each

$4 over the threshold for one child, and $2 for each $4 over the threshold for two or more

children. For married couples, a joint return must be filed to claim the credit. If the credit

household); Minn. Stat. § 290.06, subd. 6c(c) (state head of household status tied to qualifying under federal law).

This would probably increase their costs beyond any state marriage penalty savings.

20

The credit could result in a marriage penalty in a second way. If two individuals have three or more

dependents between them, the limit of $1,440 may reduce the credit the two individuals could claim if they marry.

However, to qualify for a credit, the taxpayer must “keep a home.” See I.R.C. § 21(e) (paying half the cost of

“maintaining a household” required); Minn. Stat. § 290.067 (state credit tied to federal amount). This requires the

taxpayer to pay over half the cost of running the home during the year. Thus, an unmarried couple who cohabitate

could not each qualify for a credit. But they are also likely to realize offsetting savings in housing and other costs

from combining their households. As a result, we have not included these situations in calculation of marriage

penalties or maximum amounts. This situation is similar to the head of household filing status.

21

Under the scenario outlined in footnote 20, marriage may result in the loss of more than the maximum

amount of the credit. Assume C and B each have two dependents, spend over $6,000, and have $21,880 of

household income. As a result, they each qualify for a dependent care credit of $1,440 or a total credit of $2,880.

They marry. Their combined income is now sufficient to put them over the limit for which they can qualify for any

credit in tax year 2006. As a result of joint filing, their tax increases or benefits decline by $2,880. As noted in

footnote 20, they could not qualify for this amount if they maintained a common household without marrying; it also

seems unlikely that they would spend $6,000 on dependent care given total household income of $17,400 each.

22

Within these limits, a maximum of $200 per family of computer hardware and software applies. Minn. Stat.

§ 290.0674, subd. 1(3).

House Research Department Updated: July 2007

Marriage Penalties and Bonuses and the Minnesota Income Tax Page 16

exceeds the amount of tax, a refund is paid. The education credit can create marriage penalties

because marriage may cause the income limit of $33,500 plus the phaseout range to be exceeded.

Because there is a relatively short phaseout range ($4,000 of income for parents claiming the

credit for one or two children), a small amount of additional income resulting from the marriage

may result in loss of the entire credit.

The maximum marriage penalty is $1,000 multiplied by the number of children for whom the

credit could be claimed prior to marriage.

23

Because the credit is refundable, it does not create

marriage bonuses.

Long-Term Care Insurance Credit

The income tax allows a credit for premiums paid for long-term care insurance. The credit

equals 25 percent of the premium paid up to a maximum of $100 or $200 for a joint filer.

Because the maximum credit for married filers is twice the maximum for a single filer, no

marriage penalty can result. However, because the credit is not refundable, it may provide a

marriage bonus.

24

The maximum marriage bonus is $100.

25

Working Family (Earned Income) Credit

The working family credit (WFC) follows the federal earned income credit in its structure. It

provides a refundable credit equal to a percentage of earnings up to a maximum amount. The

credit rate increases if the taxpayer has one dependent, and it increases further for two

dependents. The credit is taken away or phased out as earnings or adjusted gross income rise

above a threshold amount. The threshold amount is $2,000 higher for married joint filers than

for head of household filers, which reduces the marriage penalty for couples whose combined

income is within the phaseout for heads of households. For heads of household, no credit is

available in tax year 2007 for adjusted gross income above $37,729; this limit extends to $39,729

for married couples. Eligibility for the credit is eliminated, if the taxpayer has modest amounts of

unearned income ($2,900 in tax year 2007), such as interest, dividends, rents, or capital gains.

Most of these dollar amounts—the earnings qualifying for the credit, the limit on unearned

income, and the rates for phasing out the credit—are the same for married and single filers, while

the income thresholds for phasing out the credit is $2,000 higher for married filers than for single

filers in 2007. As a result of these dollar limitations, the WFC can result in marriage penalties or

bonuses in several ways.

23

For example, a $6,000 marriage penalty would occur if two individuals, each with three dependents, receive

the maximum credits (i.e., $3,000 each), marry each other, and the combination of their incomes results in their joint

income exceeding $45,500 (the end of the phaseout range for six dependents). They will lose all the credits

($6,000).

24

One spouse may not have sufficient tax liability to take full advantage of the credit; marriage may permit the

tax liability of the other spouse to be used to claim part of the credit.

25

The marriage bonus occurs when one spouse pays long-term care premiums, but does not have sufficient tax

liability to claim the full credit that otherwise would be available and marriage results in sufficient tax to claim an

increased credit. Assume C pays $400 in long-term care premiums, but has no Minnesota tax liability because her

taxable income is too low. C marries B who has $200 of Minnesota liability. As a result C’s payment of long-term

care premiums now qualifies for the full $100 tax credit.

House Research Department Updated: July 2007

Marriage Penalties and Bonuses and the Minnesota Income Tax Page 17

•

Marriage and the combining of both spouses’ incomes may result in more income being

in the phaseout range, reducing or completely taking away the credit.

• Marriage may put the couple over the maximum threshold for unearned income, taking

away the entire credit.

• Marriage may enable a low-income earner to qualify for a larger credit, because his or her

spouse has dependent(s) and little or no earnings. Adding one or two dependents may

allow the wage earner with one or no children to qualify for a higher credit amount.

• Marriage may enable a low-income earner to qualify for a larger credit because his or her

earnings alone were not sufficient to reach the maximum credit.

The maximum marriage penalty is loss of the entire credit or $3,302 for tax year 2007.

26

The

maximum bonus is $1,651.

27

Alternative Minimum Tax (AMT) Exemption Amount

The alternative minimum tax or AMT is an alternative tax that applies if it yields a higher

amount than the regular tax. It is calculated at a flat 7-percent rate on an expanded tax base as

compared with the regular tax. The only deduction is an exemption amount that varies with

filing status. The AMT generally applies to individuals and couples who have relatively large

amounts of deductions, exclusions, and other preference items, such as itemized deductions,

accelerated depreciation, and so forth.

The AMT exemption is $62,300 for married joint filers and $46,750 for single filers in tax year

2007. Because the exemption for married joint filers is not twice the amount for single filers, it

can result in a marriage penalty. Similarly, the AMT and the exemption can also result in a

marriage bonus.

28

The maximum amount of the potential penalty equals $1,997 for a married couple.

29

The

maximum amount of the potential marriage bonus is $995.

30

26

In theory, two individuals who marry can each lose the maximum credit. Assume C and B are single parents

and each has two qualifying children and $20,000 of earnings. They qualify for the maximum working family credit

of $1,651 each. If they marry, their joint income is $40,000, which is above the point where the credit is fully

phased out for married filers. They pay a marriage penalty of $3,302.

27

Assume that C has two qualifying children, but no earnings. C receives no WFC because C has no earnings.

B has $20,000 of earnings and no qualifying child. B qualifies for no WFC, since the credit for single filers without

a qualifying child is phased out at less than $13,000. Marriage of C and B allows the couple to receive the

maximum credit of $1,651.

28

The structure of the AMT can yield a bonus, if one spouse has a high regular tax and the other spouse would

(if filing as single) be subject to the AMT. The regular tax liability generated by the second spouse’s income

eliminates the AMT that otherwise would apply to the first spouse’s situation in filing a single return. There may be

offsetting penalties under the regular tax.

29

Two single taxpayers would qualify for $46,750 of exemptions each for a total exemption of $93,500. If

they married, their exemption would drop to $62,300. The rate under the AMT is 6.4 percent, so the maximum tax

increase equals $1,997 ($93,500 - $62,300 x 6.4%).

House Research Department Updated: July 2007

Marriage Penalties and Bonuses and the Minnesota Income Tax Page 18

Phaseout of the AMT Exemption

The law phases out or takes away the AMT exemption for alternative minimum taxable incomes

over threshold amounts. These amounts vary by filing status. Because the threshold amounts for

married joint filers are not twice the width for single filers, these thresholds may increase taxes

as a result of two individuals marrying. The threshold is $112,500 for a single or head of

household filer and $150,000 for a married joint filer.

The maximum amount of the potential penalty equals $1,200 for a married couple.

31

The

maximum amount of the potential marriage bonus equals $600.

32

Features of Federal Law that Create Minnesota Penalties

and Bonuses

A number of features of the federal income tax create marriage penalties or bonuses that

carry over to the Minnesota individual income tax.

Marriage penalties and bonuses under the Minnesota income tax also result from the close links

between the state tax and the federal income tax. Calculation of Minnesota taxable income

begins with federal taxable income. Taxpayers take the amount of federal taxable income from

their federal return and then make a few modifications to determine Minnesota taxable income to

which the tax rates apply. As a result, many deductions and exclusions under federal law

determine the amount of state taxable income. For example, itemized and standard deductions,

deduction of capital losses, and retirement savings deductions (e.g., 401(k) plans, IRAs, and so

forth) are determined by federal law for state purposes.

Many of these calculations are subject to fixed dollar limitations. In some instances, these dollar

limits can result in marriage penalties, marriage bonuses, or both. For example, the income level

at which Social Security benefits begin to be subject to tax for single filers is $25,000 and for

married joint filers is $32,000 ($18,000 less than twice the amount for single filers). These fixed

amounts can result in either marriage penalties or bonuses, depending upon the income-split

30

If one spouse has no AMT income over the exemption amount, while the other spouse has AMT income that

is $15,550 or more below the exemption, marriage effectively increases the exemption by $15,550. The exemption

is $46,750 for a single and head of household filer and $62,300 for a married joint filer. The marriage bonus in this

case equals $995 or the $15,550-increase in the exemption multiplied by 6.4 percent rate. A larger marriage bonus

could result from the situation described in footnote 28, if one spouse has a high income subject to regular tax and

other has substantial AMT liability.

31

If the couple were able to file as single taxpayers, they would have an additional $75,000 of AMT income

before their exemption would begin to phase out. Two single filers would each have $112,500 thresholds or a

combined threshold of $225,000. The phaseout threshold drops to $150,000 if the individuals marry. Since the

phaseout rate is 25 percent and the tax rate is 6.4 percent, the maximum penalty amount equals $1,200.

32

If one individual has AMT income that is over the threshold and the other has AMT income that is $37,500

or more below the threshold, the married joint threshold has the effect of increasing the threshold for the married

couple by $37,500 (i.e., from $112,500 to $150,000). The value of this increase equals $600 ($37,500 x 25% (the

phase-out rate) x 6.4% (the tax rate)).

House Research Department Updated: July 2007

Marriage Penalties and Bonuses and the Minnesota Income Tax Page 19

between the spouses. For example, if each spouse has $25,000 of income, the lower threshold

for including benefits in taxable income for joint filers increases the married couples’ taxable

income by $11,100.

33

By contrast, if one spouse was in the workforce and not receiving benefits

and, thus, would not have benefited from the $25,000 floor on inclusion of benefits in taxable

income, the couple receives a marriage bonus, because marriage increases the amount of

provisional income necessary to trigger inclusion of benefits in taxable income to $32,000.

Numerous provisions of federal law carry over to state law and can result in marriage penalties

or bonuses under the state tax. In 1996, the General Accounting Office (GAO) catalogued 59

provisions of the federal income tax where tax liability depends upon marital status and, thus,

can result in penalties or bonuses.

34

Of these 59 provisions, some do not carry over to calculation

of the Minnesota tax because they affect credits, rates, or other tax features that do not flow

through to Minnesota tax. However, 42 appear to flow through to Minnesota tax.

35

Since the

GAO report was prepared, Congress has enacted several tax bills. These bills have modified

some of the affected provisions and have enacted new provisions that create penalties and

bonuses.

36

The legislature has opted to conform to federal income tax provisions for a number of reasons.

Perhaps the most important of these is simplicity and ease of compliance and administration for

both taxpayers and the Revenue Department. Since most individuals must comply with the

federal tax, adopting its provisions greatly simplifies compliance with the Minnesota tax.

Adopting an approach that deviates from federal law on these basic tax base calculations could

have a high cost in additional resources for individuals to comply with the law. This was one of

the major complaints about the pre-1985 Minnesota tax that differed substantially from federal

law, including using individual filing rather than joint filing by married couples, the major source

of penalties and bonuses.

33

For married joint filers, the amount of Social Security benefits included in taxable income equals 50 percent

of the first $12,000 of provisional income (adjusted gross income other than Social Security benefits, plus tax-

exempt interest and half of Social Security benefits) over $32,000, and 85 percent of provisional income over

$44,000, up to a maximum of 85 percent of benefits. For single filers, 50 percent of the first $9,000 of provisional

income between $25,000 and $34,000 plus 85 percent of provisional income over $34,000 is included in taxable

income. Thus if two single filers with $25,000 of provisional income each marry, they move from having no

benefits included in taxable income to having up to $11,100 of benefits include in taxable income (50 percent of the

$12,000 of provisional income between $32,000 and $44,000, plus 85 percent of $6,000 of provisional income

between $44,000 and $50,000). The actual amount included in taxable income would be limited to 85 percent of

benefits. This example assumes that each single filer received higher Social Security based on individual earnings

rather than on the spousal benefit; in many cases couples would experience an increase in the amount of benefits

received as a result of marriage.

34

General Accounting Office, Income Tax Treatment of Married and Single Individuals, September 1996.

35

The marriage penalty or bonus potential of most of these provisions is minor. Some affect few taxpayers.

For others, the likelihood that they result in marriage penalties or bonuses seems low. It does, however, point out

the pervasiveness of the phenomenon.

36

See, e.g., Adam Carasso and C. Eugene Steuerle, How Marriage Penalties Change under the 2001 Tax Bill

(Washington, DC: Urban Institute, 2002) (estimating changes in penalty amounts).

House Research Department Updated: July 2007

Marriage Penalties and Bonuses and the Minnesota Income Tax Page 20

Estimates of Federal Penalty and Bonus Amounts

Estimates have been made of the amount of federal marriage penalties and bonuses; tax return

data is not now available to make similar estimates of the Minnesota penalties and bonuses.

Both the Congressional Budget Office

37

(CBO) and economists in the Office of Tax Analysis

(OTA) in the Treasury Department

38

have estimated the amount and distribution of marriage

penalties under the federal income tax.

39

These two studies use slightly different methodologies

and data in measuring marriage penalties and, as a result, reach somewhat different results.

40

Neither study takes into account behavioral responses to the marriage penalty (see the discussion

in the next section). They simply calculate the increase or reduction in tax resulting from joint

filing under a series of assumptions about what the tax would be if the each spouse could file a

single return.

Congressional Budget Office Study.

41

The CBO found (for tax year 1996) that 21 million

couples paid marriage penalties of a total of $29 billion, while 25 million couples received

bonuses totaling $33 billion. Three million couples were unaffected. Those paying penalties

comprised 42 percent of married filers and those receiving bonuses 51 percent. Lower

income couples were more likely to receive bonuses, while higher income couples were

equally likely to receive bonuses or pay penalties. Marriage bonuses and penalties for higher

income couples are higher in dollar amounts, but constitute smaller amounts as a percentage

of income than those of lower income couples. For example, the average marriage penalty

for couples with incomes over $100,000 was $2,600 or 2 percent of income. The average

penalty for couples with incomes below $20,000 was $800 or nearly 8 percent of income.

42

Study by economists in the Treasury Department, Office of Tax Analysis.

43

The OTA

economists found (for tax year 1999) that 24.8 million taxpayers or 48 percent had marriage

penalties, while 21 million or 41 percent had marriage bonuses. The aggregate penalties

were $28.3 billion and bonuses $26.7 billion. As can be seen, these estimates differ

37

See CBO, For Better or Worse, 27-36.

38

Nicholas Bull, Janet Holtzblatt, James R. Nunns, and Robert Rebelien, Assessing Marriage Penalties and

Bonuses (Proceedings of the 1998 National Tax Association’s Annual Meeting, 327-40).

39

In addition, a number of other published studies by nongovernmental economists have been done. See, e.g.,

James Alm and Leslie Whittington, “The Fall and Rise of the Marriage Tax,” National Tax Journal 49 (1996): 571;

Daniel Feenberg and Harvey Rosen, “Recent Developments in the Marriage Tax,” National Tax Journal 48 (1995):

91.

40

CBO used published data from the SOI, Statistics of Income, and census data, while the OTA economists

used a sample of actual tax returns. In addition, they used different techniques for measuring marriage penalties and

bonuses.

41

CBO, For Better or Worse, 27-36. The study computes marriage penalties and bonuses using several

different methods. The text summarizes the amounts calculated using the “basic” measure, rather than the broader

or narrower alternatives.

42

Ibid., 33-34.

43

Bull, et. al, Assessing Marriage.

House Research Department Updated: July 2007

Marriage Penalties and Bonuses and the Minnesota Income Tax Page 21

somewhat from the CBO numbers. The OTA economists find more taxpayers paying

penalties and fewer receiving bonuses. As with CBO’s results, marriage penalties

predominate at higher income levels, whereas bonuses are more common at lower incomes.

44

The OTA economists also estimated the amount of the “singles penalty”—i.e., the additional

tax paid by unmarried filers because they are not allowed to file married joint returns. This

amount was $30.2 billion and affected 40.5 million filers.

45

Since the OTA and CBO studies were done, Congress has enacted tax changes that clearly have

generally reduced marriage penalties and increased marriage bonuses under the federal income

tax. In particular, the Economic Growth and Tax Relief Act of 2001 (EGTRRA) was explicitly

directed, in part, at reducing marriage penalties. For example, EGTRRA made the married joint

standard deduction twice the single amount (gradually in steps) and increased the width of the

married joint 10- and 15-percent rate brackets to be twice the amount for single filers. A study

by the Urban Institute has characterized these changes as creating “less of marriage penalty or

more of a subsidy at most household incomes and at most income shares for the secondary

earner.”

46

Estimates of marriage penalties and bonuses under Minnesota law have not been made. The

current income tax sample data indicates the amount of income earned by each spouse, but

estimating penalties would require making assumptions about which spouse received unearned

or investment income. Nevertheless, several conclusions probably can be safely made regarding

the amount of Minnesota marriage penalties relative to the federal estimates:

• State penalties and bonuses are much smaller both in absolute terms and relative to the

tax burden, compared to those under the federal tax. First, the Minnesota tax rates are

much lower. Second, the relative differences in tax rates are much smaller; the rate

structure is flatter. Third, there are fewer rates and less progression.

• Penalties and bonuses under the credits (particularly the working family credit) are likely

to be a bigger factor in overall penalties than the rate structure (as compared with federal

law). These credits provide larger penalties (and bonuses) in absolute dollars than the

rate structure. By contrast, the federal penalties from the rate structure are larger. The

penalties under the state credits likely affect fewer taxpayers, but the amounts and

percentages of incomes are much larger for those affected.

• The penalties that carry over from federal law—particularly the phaseout of itemized

deductions and personal exemptions—are likely significant factors in creating state

marriage penalties and bonuses. Prior to federal changes that increased the standard

deduction for married filers to be twice the amount allowed for single filers, the standard

deduction also was a significant factor in creating state penalties and bonuses. But

penalties that flow through from the federal law are not as large as those caused by the

state tax rate structure. However, they do make up a larger share of state marriage

44

Ibid., 9-10.

45

Ibid., 10.

46

Carasso and Steurele, How Marriage Penalties. This study focuses on the effects on households with

incomes of $80,000 or less.

House Research Department Updated: July 2007

Marriage Penalties and Bonuses and the Minnesota Income Tax Page 22

penalties (and bonuses) than the standard deduction previously did of federal marriage

penalties (and bonuses).

47

Behavioral Effects of Penalties and Bonuses

Studies suggest that marriage penalties and bonuses may affect taxpayer behavior—

particularly decisions by secondary earners to work and in some limited instances,

marriage decisions.

Economists have studied whether marriage penalties under the federal income tax affect the

behavior of taxpayers.

48

The studies have focused on two potential effects of marriage penalties:

• Labor supply effects. Do marriage penalties or bonuses reduce (or increase) the extent

to which married individuals work? Joint filing can result in the application of higher

marginal tax rates. This is particularly true for the second earners; their spouses’ incomes

under joint filing can put them in higher tax brackets.

49

These higher tax rates mean that

the after-tax return for taking a job or working more hours will be lower (i.e., the wages

or salary remaining after taxes are paid will be less). A reasonable inference is that these

higher marginal tax rates will cause some people to work less. One would expect that

these higher marginal tax rates cause some individuals to substitute “leisure,” staying

home to care for young children or other activities, for paid work. Marriage bonuses

could also reduce work effort. Marriage bonuses raise the after-tax wages of the primary

earner. This additional income may induce either or both spouses to work less.

Several empirical studies have been done of these labor supply effects of the marriage

penalties and bonuses under federal law. They find somewhat varying and mixed effects.

The studies generally have found that second earners respond more strongly to incentive

effects of the marriage penalty and bonuses—i.e., the marriage penalty reduces the

amount of work by second earners (typically wives). The Congressional Budget Office

47

The increase in the federal standard deduction amounts for joint filers to equal twice that for single filers

reduced federal revenues by about 21 percent of the cost of doubling the rate bracket widths. See Bull, et. al,

Assessing Marriage. By contrast, doubling the state standard deduction amounts to twice the single amounts would

cost slightly more than 56 percent of doubling the rate brackets, based on House Research’s calculations.

48

The authors are aware of no published studies of the effects of marriage penalties under state income taxes.

As a practical matter, many state income taxes are marriage neutral or relatively marriage neutral. They either use

individual filing regimes or have flat tax rates. See Appendix B for a summary of how other state income taxes treat

married couples relative to singles. Second, because state tax rates and burdens are significantly lower than the

comparable rates and burdens under federal law, the magnitude of penalties will be much smaller. However, it

seems likely that state taxes, to the extent they impose similar penalties, will reinforce any effects under federal law.

49

To illustrate, assume that C and B are married. C earns $50,000. If B earns a dollar of income it would be

subject to a federal marginal tax rate of 25 percent and a state marginal rate of 7.05 percent (assuming the couple

claims the standard deduction) because it is added to C’s income under the joint filing method. By contrast, assume

B is single and earns either $7,000 or $20,000. (The impact of credits and the Social Security tax are ignored here.)

B’s marginal rate is either 0 (for $7,000 since it is less than the standard deduction and personal exemption amount)

or 20.35 percent (15% federal + 5.35% state). The increase to B’s marginal rate as a result of her marriage to C is

32.05 percentage points (25 + 7.05) where B earns $7,000 and 11.7 percentage points (25 + 7.05 = 32.05 compared

with 15 + 5.35 = 20.35) for $20,000.

House Research Department Updated: July 2007

Marriage Penalties and Bonuses and the Minnesota Income Tax Page 23

found in a simulation of the effects of marriage penalties and bonuses on work effort that

the joint filing caused higher earning spouses to increase their work by a small amount

(0.l percent to 0.3 percent) and secondary earning spouses to reduce their work by a much

larger amount (4 percent to 7 percent).

50

• Marriage decisions. Do marriage penalties and bonuses affect the decision whether to

marry or divorce? Bonuses and penalties provide financial incentives in some instances

to marry, not marry, or divorce, depending upon the circumstances of the individuals. It

is conceivable that they have measurable effects on these decisions.

Economists have done a few studies of these possible effects. One study found that the

marriage penalty had a small, but significant, effect on the rate of marriage.

51

By

contrast, another study found no significant effect on the decision to marry, but did find

that the marriage penalties had a statistically significant effect on the timing of

marriage—i.e., it caused some couples to delay when they married.

52

A third study found

that the treatment of marriage under the state and federal earned income tax credits

affected marriage decisions.

53

These studies have all been done relatively recently and it

seems safe to conclude that any effects of the federal income tax penalties on marriage

decisions are small at best. The state marriage penalties are much smaller, of course, so

their effects (taken alone) are likely to be of no significance, but they may reinforce the

effects under the federal tax.

50